Want to learn more? Check out my book, Start, Manage & Exit A Profitable Government Contracting Firm.

Welcome back for Part II!

Last post we discussed the various type of contracts (Firm Fixed Price, Time & Materials, and Cost Plus Fixed Fee) and started to get into what we call indirect cost “pools” – Fringe, Overhead and General & Administrative. For this post, we will delve a bit further into what makes up the “pools”, how they are approved by the government and how you use the pools to develop the price per hour you can charge to the government.

So what make up these so called “pools”? On this hot summer day as I write this I wish they were cool places to dip your toe. Alas, they are simply categories of expenses….

Imagine that you have three boxes and a huge pile of receipts. Your accountant would prefer you file the expenses into various “types” of expenses or the three boxes rather than the big pile and the government is no different. Each company can decide exactly how to divide their expenses but this is the most common approach:

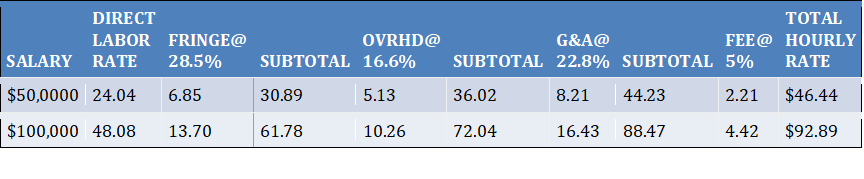

Direct Labor Rate. This is easy. You take the salary of the person you are proposing and divide by 2,080 (the number of hours in a year). For example, if you pay someone $50,000 per year, their Direct Labor Rate is $24.04.

Indirect Costs. Indirect Costs are anything that you cannot directly charge to the government such as paying for the employee’s health care premiums or items like rent, accountants or paper for the copier. This is the complicated part and I’ll explain a bit more in depth below.

Fee which is your Profit on the task. This is negotiated within your proposal and can be either a fixed number ($1,000) or a percentage of the billed amount (5%).

So… back to the Indirect Costs. Indirect Costs are further broken into sub pools (or categories). The most common approach to this division is:

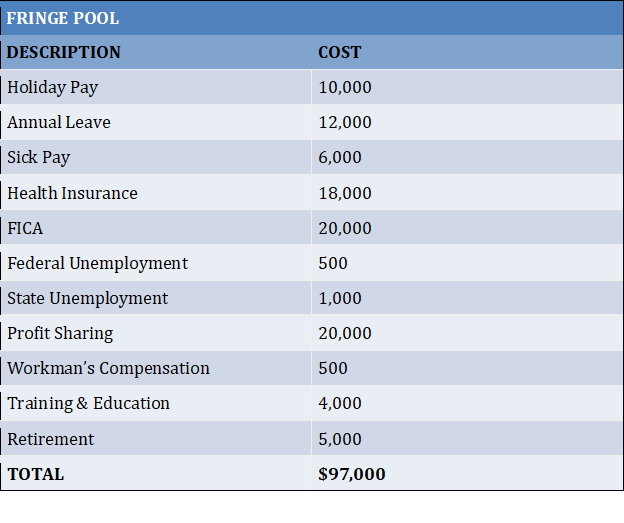

Fringe Pool – items such as health care, retirement contributions, vacation, sick, and workman’s compensation.

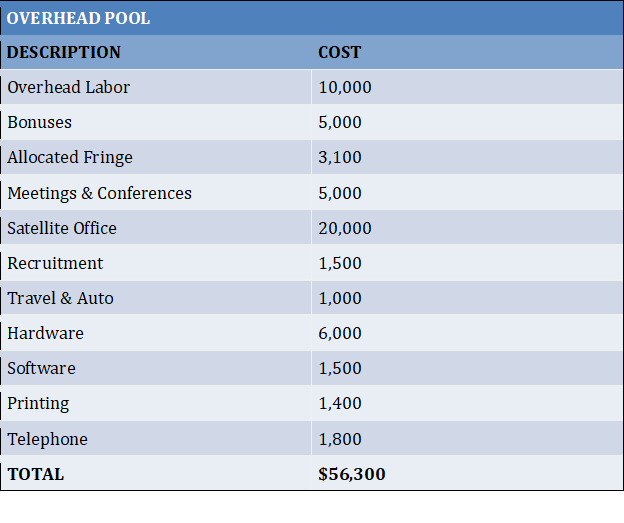

Overhead Pool – items that cannot be billed directly to a contract but can be attributed to the cost of doing business with one or more customers. For example, computers, rent for billable employees, salary paid to an employee between two projects or utility costs for space allocated to billable employees.

Some companies divide their Overhead Pool into two distinct pools: one for Company Site Employees and one Government Site Employees. This is because it obviously costs us more in overhead costs to employee someone who works on our site than on a government site. It doesn’t seem fair to allocate (and thus charge) costs for Company Site employees to clients who are providing those materials such as desks, space to work and computers for us.

General & Administrative — items that attributable to running your business in general. Examples include the salary of the President of your company (unless the President is a billable employee and then you should divide the salary proportionately into the correct pools), rent for the area where administrative personnel work, accountant and lawyer fees.

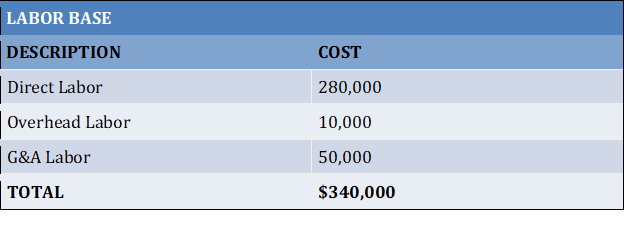

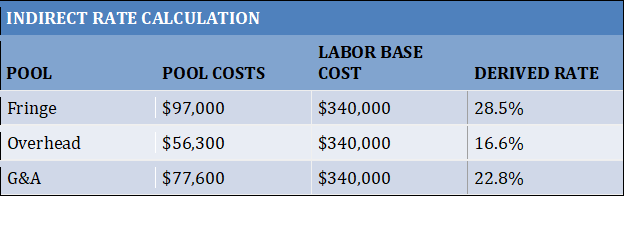

Once you have divided your costs into their various pools, you can calculate percentage costs for each pool based on the total Direct Labor costs. See the charts below for a very simplified sample budget and the corresponding “Indirect Rates” that were derived.

Now, once you have your budget for the year you can start to calculate what your indirect rates are…

Let’s start with Fringe. Your total cost for Fringe is $97,000 and your total Labor Base is $340,000. To compute your Fringe Rate you divide Fringe by the Labor Base total for a percentage of 28.5%.

The other indirect rates are calculated using the same methodology as you can see below.

Once you have the indirect rates, you can use them to create your Cost Plus Fixed Fee rates that you bill to the government.

Your proposed budget and indirect rates are submitted to the Defense Contracting Auditing Agency (DCAA) at the beginning of the year and are called Provisional Rates. DCAA will either approve or request a change to what you proposed. Once they are approved you can use those indirect rates to bill the government on your CPFF contracts.

Provisional Rate are just that … provisional. They are based off what you propose in your budget. You do your best to stay within the budget but things happen and your actual numbers are sure to not exactly match the budget. At the close out of the contract you will apply your actual indirect rates (based on your actual expenditures) to the direct labor expended and do a reconciliation between what was billed and the actual costs incurred on the contract. At that point, you will either owe the government back some money (if they were lower than budgeted) or you can attempt to collect additional fees from the government (if they were higher than budgeted).

So… that is your quick overview of how to create a government contracting budget and how it is used to create Cost Plus Fixed Fee rates. This is an immensely simplified view to give you a basic understanding. If you have questions or need further explanation please contact us for our business consulting services.

Leave a comment